September 2014: Financing is an ongoing challenge for all Biotech companies. Without sufficient resources, products cannot be advanced in the development. Scarce resources help companies to focus as it is more important to bring one or two products into the clinic than advancing five different programs in pre-clinical development. But many European companies are struggling to raise sufficient capital even for their lead products and financing remains a key limiting factor for European biotechs.

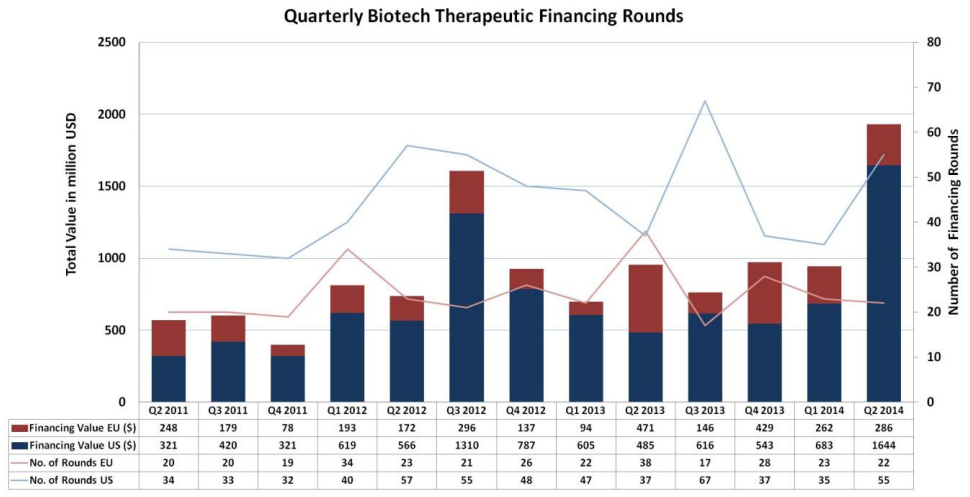

If we compare financing in Europe with the US, we can see that private therapeutic and diagnostic companies in the US in Q2 2014 had the highest amount of money raised in the last three years with USD 1.6bn. However, in Europe the USD 262 m raised in Q2 2014 is below the 3 year average of around USD 340m per quarter. So that is six times more investments into private therapeutic Biotech companies in the US versus Europe where both regions account for about the same number of companies (963 in the USA and 814 in Europe according to Biotechgate).

If we consider the number of financing rounds, one notices that over the past 3 years, the average number of financing rounds per quarter was 24 in Europe and 44 in the US. So the average amount raised by a US private therapeutic company is USD 31m versus USD 14m in Europe. Thus, European companies have to spend more time with fundraising as on average they receive only half the amount per round compared with their US peers.

So how can European companies increase their chances to attract sufficient resources? There are different ways to finance innovation:

Services

Many companies are offering services based on their technology platform or know-how to have sufficient income to keep the company going. Even though this can be an interesting way to survive, most often the income and profit margin is not sufficient to fund pre-clinical or clinical work. Thus, this could be helpful in early stages of development or to bridge a period where no investment can be found. However, it often distracts the company from focusing on real value creation – advancing their lead product.

Licensing Income

Venture Valuation recently published an article in Nature Biotechnology 32, 617–619, (2014) based on data from its Biotechgate deals database looking at the difference between big pharma and SMEs in the upfront payments. It was shown that the up-front amount is sensitive to the stage of the product and that on average big pharma would pay higher amounts than small and mid-size biotech companies (SMEs). Thus out-licensing a product can be a very interesting source of capital, more so if big pharma is the partner. If the company can out-license a second or third product and try to keep the rights on its lead product for as long as possible then this is most promising. Investors often focus on the lead product and do not put a lot of value on products further down the pipeline. This effect can be seen when analyzing the value increase of publicly listed companies that out-license 3rd or 4th products in their pipeline. So choosing the right partner and the right strategy is crucial.

Equity and Grant Funding:

Equity funding through VCs is the classic way of financing a therapeutic biotech company. However, there are also different strategies and sources for equity and grant financing.

a) Is Orphan saving Biotech?

Orphan drugs have been en vogue for a while. However, early 2014 has been a record financing that puts drugs for small patient population even more on the map. In Q1 2014, over 60% of the financing in European Biotech have gone to companies that have a lead Orphan drug product. Over USD 170 m of the recorded USD 257 m in European Biotech financing have been done by orphan focused companies. Dutch UNIQURE raised USD 91 m and French Txcell raised USD 22 m in an IPO, but also Swedish Wilson Therapeutics raised USD 40 m this year from VCs. So is Orphan saving the Biotech industry? It does certainly look like it’s an interesting investment possibility for Venture Capital investors. Of the current 43 brand blockbusters, 18 were approved solely for orphan, so this shows the big potential.

Never the less, Orphan drugs provide great opportunities for Biotechs in terms of raising capital / IPOs, by out-licensing to big pharma but also for M&A exits. The recent merger of BioAlliance Pharma SA, France with Topotarget A/S, to become Onxeo – The Orphan Oncology Innovator, underlines this trend.

b) Alternative equity/grant funding

When fundraising for a company, it is helpful to think outside the box and try to identify alternative funding sources. Just going for the obvious VC investor is not good enough. The company’s strategy, amount of required funding or business model may not fit the initial targeted venture capital investor. There are a number of other sources available like Business Angel Groups, Corporate Venture Capital, Endowments/Foundations, Family Office/Private Wealth Funds, Government Organizations, Hedge Funds and Private Equity. The key is actually to be able to identify such investors. They may not be an obvious choice and often stay in the background. So there are different ways to identify such investors: 1) check your peers to see where money is coming from. Who has made recent investment/provided grants in the area that you are active in. Maybe not direct competitors, but peer groups. 2) Use support provided by local government organisations. Many countries provide companies with support in accessing capital. There are also a number of European initiatives such as Fit for Health 2.0 (www.fitforhealth.eu) that help companies attract grants and private funding. 3) Use information sources like Biotechgate which has a database with thousands of life sciences investors interested in investing in various aspects of the industry or use websites of business angels and venture capital associations. In any case of fundraising, quality is far more important than quantity.

At the end, fundraising is a key task of management of every biotech company. Resources (time and finance) have to be allocated for the fundraising process. Only a professional approach will lead to success. Relying on chances and the hope that investors will knock on your door, materialize only seldom. Plan enough time for the fund-raising – it will not happen overnight and have a plan B (and C) available so you are not totally dependent on having the money in the bank tomorrow – which puts the company in a very bad negotiation position. Know your strengths, but also your weaknesses and know how to overcome them. Be aware of the value of the company and how much equity you are willing to give away for the amount you are looking for. Use as much as possible non diluting financing such as grants. Know how much money you are raising and what you will do with the money. At the end, an investment will put the investor into the same boat as the company, both looking to bring the company to success. So choosing an investor is like getting married – its an important decision.

Author: Dr. Patrik Frei, CEO Venture Valuation

September 2014

Also published in European Biotechnology: http://www.hornonline.com/books/european_biotechnology/#18