Does it make sense for a life science fundraising executive in Europe to look internationally for early-stage funding? Should U.S. based firms look at investors in Europe and Asia? As the famous folk singer Bob Dylan sang “the times they are a changing” and the answer is yes!

To someone looking to fund a life science startup ten years ago, the funding possibilities would have been primarily local. Government programs and angel networks are almost invariably regionally-focused, as are many VCs (particularly within the long tail of smaller VC funds that used to provide capital to life science start-ups, many of which have now closed their doors). However, the new investors on the stage today are typically much broader in scope. Large pharma companies and global PE companies that used to focus on mid to late-stage opportunities are now looking to capture the value of emerging technologies; from the opposite direction, medical foundations that used to support only basic biology research are now focusing on getting new breakthroughs out of the lab and into the marketplace, and while some foundations are regionally based, many are looking for advancements in their field globally. Family offices, too, are most often interested in opportunities worldwide.

To an entrepreneur unaware of how the world has changed around him, regional investment can become a self-fulfilling prophecy; the entrepreneur will focus their fundraising campaign on the traditional, mostly regional sources, and never reach out to the new global investors that might be very interested in the opportunity.

LSN Research in collaboration with Venture Valuation, Biotechgate Database has examined the geographical scope of the investors who take part in early-stage life science deals. We looked at the trove of financial data available via the BTG Company Platform, and took a sample of small financing rounds ($10m or less) raised by companies developing a preclinical or Phase I therapeutic product. From this sample, we aggregated a list of all the lead and co-investors who had participated in these deals, and then we took a more detailed look at each of these investors and assessed the range of their activities. To keep things simple, we categorized the scope of each investor’s allocations as

- Global, anywhere on the planet where companies are a fit for investor.

- Continental, North America, Europe or Asia.

- Regionally, focused on small discrete geographies like Massachusetts, California, or specific countries in Europe.

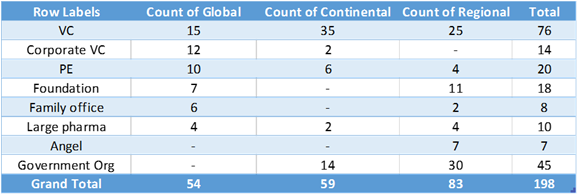

Sample 1: From Biotechgate Company Database

Lead and Co-investors that have Allocated <$10 Million to Pre-clinical or Phase I

As you can see, about 25% of the investors that are active in these early stage deals reported in BTG financing rounds database are global investors. To further support this, we also pulled data from investors in the LSN Investor Database who are willing to allocate under to $10 million in a single round into Pre-clinical and Phase I stage therapeutics companies.

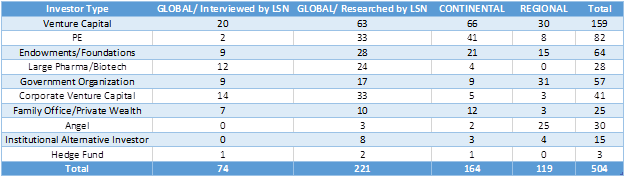

Sample 2: From LSN Investor Database

Investor that are willing to Allocate under $10 Million and are looking at Pre-Clinical and Phase I

Early Stage life science investment is in transition. This means that there is a clashing of the old ways and methodologies and the generally accepted status quo. The investor available categories have morphed as new players fill the void left by the early stage VC investors. The challenge today is to get everybody singing from the same hymnal and up to speed on who’s who in the market place and educate the players on how to find the best fit for and match for capital needs. Below are 3 points to keep in mind when developing a fundraising strategy.

- Life Science fundraisers are in two camps. One camp still hangs on to out-of-date strategy that the investor market process and protocol is as follows friends and family, angels, government grants, followed by VC’s. This might have been true 5 years ago but is no longer relevant as new players have entered the arena and VCs have waned due to lack of funds and unproven track records. The new process looks more like this, friends family, angels, funding portals, government grants, followed by parsing the new investor landscape and determining who is a best fit for a fundraiser to target the old stand by and these new investors including single and multi-family offices, venture philanthropy, patient groups, corporate development, private equity, hedge funds, pensions and foundations.

- There is a self-fulfilling prophesy that says that emerging life science companies cannot canvass and get allocations from global investors and that their market place is limited to only going after regional investors. This is simply not true as it turns out that each investor type has its own modus operandi in that an angel or a regional VC strategy may be local where a venture pharma, foundation or a patient group may have no such requirement and are therefore global. Net/net is that the profile and strategy of the life science investor determines their investment sphere.

- Investors are moving upstream and this creates a trend that in turn moves investors to join in. Previously certain investor types were early stage but now when mid to late players get involved early this then creates a pull on the rest of the investor base. Basically making early stage a topic of consideration for all the mid to late stage investor categories. Investors are demonstrating that in order to remain competitive you need to form early alliances and partnerships or you will miss out. Emerging life science companies are simply forming their partnerships earlier.